Trump the Almighty, or the War Continues

July 9 was feared by everyone — investors, traders, governments, business leaders, political analysts, and the simply curious. Trump barely managed to sign a single trade agreement with the UK and slightly ease the trade war with China. After that, “warning letters” began arriving, specifying the tariff rates countries would pay for access to the U.S. market starting August 1.

Nevertheless, there is no panic-driven flight from U.S. assets.

Large capital prefers to pause until the situation becomes clearer, which has had an additional negative impact on market liquidity. Since April, huge volumes of carry trade positions have been closed in yen, franc, and euro.

It is evident that under the current U.S. tariff regime — combined with rising exchange rates of other countries' currencies against the dollar — the economic downturn in the EU, Japan, Canada, Mexico, and others will lead to dovish monetary policies. That will be the point to resume a new wave of carry trades.

The market still hopes that the EU, Japan, and Canada will manage to reach trade agreements with the U.S. before the August 1 deadline. This would boost risk appetite. Additionally, the next three weeks will be crucial in determining the Fed's policy and Powell’s fate.

There’s a chance that the U.S. Supreme Court will block the introduction of “retaliatory” tariffs (hearings begin July 31, the same day as Trump’s trade deal deadline). But in that case, Trump will shift his focus to sectoral tariffs — steel, aluminum, copper, cars, pharmaceuticals, chips, food, etc. — pushing them to extremes. This would create an entirely new market environment with no clear strategy to counter it.

A fresh election campaign will begin in the fall, and Trump risks losing control of the House of Representatives. So Donnie is rushing to score political points at any cost.

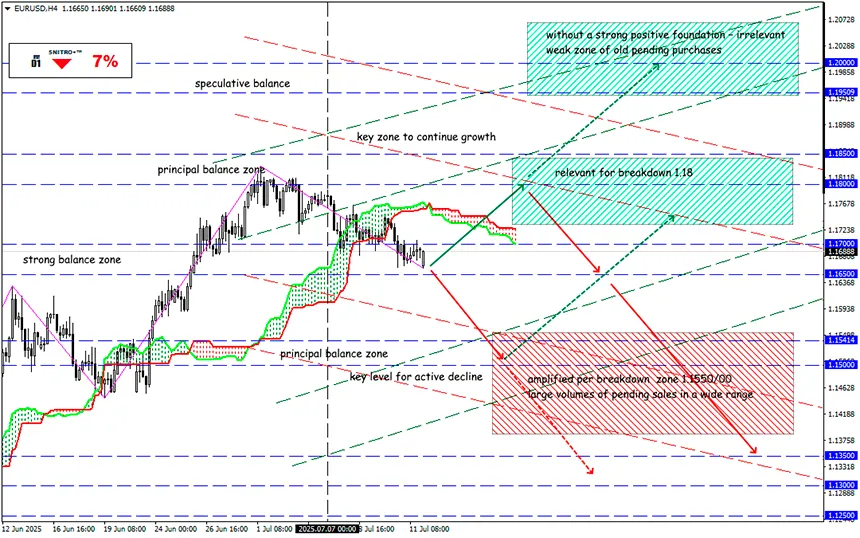

So we act wisely and avoid unnecessary risks.

Profits to y’all!